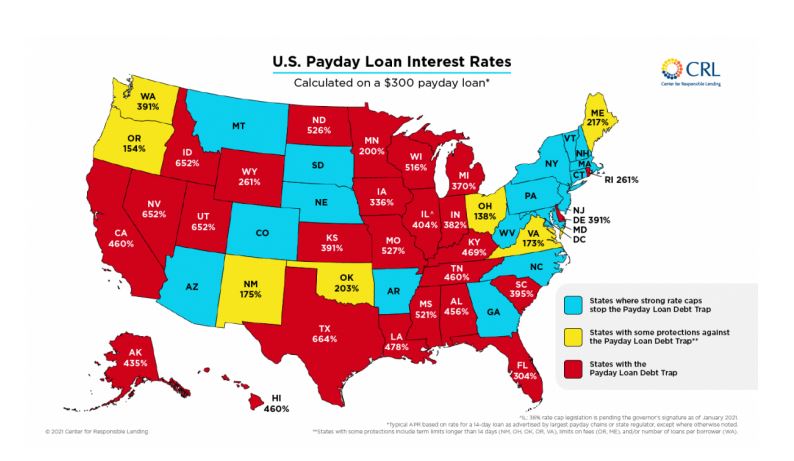

The effective U.S. payday loan interest rates, by state, for a $300 loan. In Maine, it’s 217%, the second highest in New England. Center for Responsible Lending

Desperate for cash and unable to access traditional lenders for all sorts of reasons, some Mainers turn to financial outfits that give out payday loans with terms that are sometimes impossible to pay back.

In a bid to offer better protection, state Sen. Rick Bennett, R-Oxford, told a legislative committee this week that too many Mainers are “misinformed, bilked, conned and abused by unscrupulous predator lenders, often when they are in dire personal circumstances as well and most vulnerable to snake oil and fine print.”

State Sen. Rick Bennett. Submitted photo

Bennett introduced a bill this session that would impose caps on the fees charged by lenders in the dark corners of financial services who sell money at outrageously exorbitant rates to Mainers in distress.

His amended bill would require that any fees charged are considered in calculating interest rates. Maine imposes interest rate caps on Maine-based finance companies but it doesn’t restrict fees that can accompany the loans.

The measure faces some opposition, mostly based on the reality that out-of-state firms would still be allowed to charge excessive rates to Maine residents. The bill’s future is uncertain.

In pushing his proposal, Bennett cited a complaint that a Mainer made to the federal Consumer Financial Protection Bureau as an example of the sorts of practices he aims to stop.

In that complaint, a wife said that with her husband “working minimal hours,” they were in “a very tight place” financially. She sought ought a short-term loan to get past a desperate moment.

To receive $650 immediately, the anonymous woman said, she agreed to an installment loan she hoped to pay back in two weeks, a short enough period that the interest wouldn’t be too much to bear.

What she found out, though, is that the payment plan for the loan required her to pay $150 biweekly for six months. That amounted to $1,900 to receive a $650 loan. To pay it all off after a mere two weeks required her to cough up $190 in interest as well as the principal — a 29% rate to borrow cash for half a month.

Whitney Barkley-Denney, senior policy counsel for the Center for Responsible Lending, told the Legislature’s Committee on Health Coverage, Insurance, and Financial Services that payday lenders in Maine can charge rates that reach as high as 271% annually without making any assessment of whether the borrower can pay it back. They can also seize money from borrowers’ bank accounts in their quest to recoup their loan, he said.

“This toxic combination of loan terms is the debt trap by design,” Barkey-Denney said. “The debt trap is the core of the business model.”

The state’s Bureau of Consumer Credit Protection and its Bureau of Financial Institutions told lawmakers they had no position on Bennett’s bill, but pointed out that there are “a number of limitations on the reach of the proposal and potential consequences to consumer lending in Maine that are important for the committee to evaluate as it weighs policy changes.”

Most importantly, since a 1978 Supreme Court ruling, federally-chartered banks and institutions from other states are not obligated to follow Maine’s interest rate caps and rules. As a result, the state bureaus said, Maine consumers could still face higher rates if they turn to financial entities that aren’t regulated from Augusta.

Bennett said that while it is true that “unscrupulous players are often beyond the reach” of Maine law, it doesn’t mean that policymakers in the state are helpless.

Every New England state except Rhode Island bans payday loans that charge interest rates that exceed statutory caps.

From Ohio in the West to North Carolina in the South, the only other northeastern states that top the rate charged in Maine on a $300 loan are Rhode Island and Delaware, according to the Center for Responsible Lending.

The state bureaus also warned the change might devalue Maine’s financial institutional charter and decrease lending opportunities for those considered high-risk borrowers.

“Consumers desperate for credit have options for accessibility to credit, including internet-based nonbank lenders and unlicensed payday lenders. If loans from Maine lenders are restricted, we may see residents turn more frequently to these other types of loans, which are much more difficult to regulate,” the bureaus said in their joint testimony.

Kathy Keneborus, vice president of government relations for the Maine Bankers Association, told lawmakers her group opposes the bill because it wouldn’t apply to all lenders and might limit consumers’ choices.

She raised the specter of some borrowers, unable to get small-dollar loans from Maine banks, turning to “informal loan sources” instead.

Jonathan Selkowitz, a staff attorney at Pine Tree Legal Assistance, told the panel he sees what predatory loans can do.

“Crushing consumer debt is an unfortunately common trait among Pine Tree’s client population,” he said. Too many of them “become ensnared in a cycle of debt that prevents them from using the benefits of the consumer credit market to help accumulate wealth and shed the burdens of poverty.”

“Pine Tree has observed how overwhelming consumer debt prevents Mainers from affording reliable vehicles to get to work, purchase a home, make rent, and improve their earning capacity,” Selkowitz said.

What happens, said Frank D’Alessandro, litigation and policy director of Maine Equal Justice, is that people get in over their head.

“These loans are rarely paid off with just one loan, but instead turn into multiple, repeat loans with increasing amounts of fees and interest,” he told lawmakers.

He said coping with exorbitant interest rates puts Mainers who turn to payday loans at greater risk of hunger and homelessness.

Jody Harris of the Maine Center for Economic Policy urged the committee to back Bennett’s bill, which she called “a common-sense change that would help thousands of Maine borrowers and level the playing field with other financial products.”

Legislators plan to discuss the proposed bill soon.

Send questions/comments to the editors.

Comments are no longer available on this story